is life insurance a con

Be wary of offers asking for personal information such as Social Security, bank account, or credit card numbers. Most trustworthy companies will not solicit these details when first contacting them to find out if they would like to purchase mortgage insurance to protect you from the mortgage.

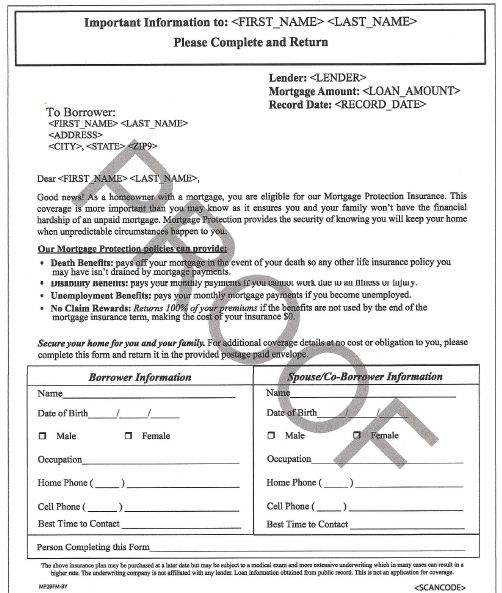

If you just recently purchased a home or refinanced your mortgage, you will likely receive many offers in the mail for "Mortgage Life Protection" or "Mortgage Life Insurance." In this article, we will take a look at the pros and cons of Mortgage Protection Insurance. You can answer the question: Is Mortgage Protection Life Insurance a scam or a smart move?